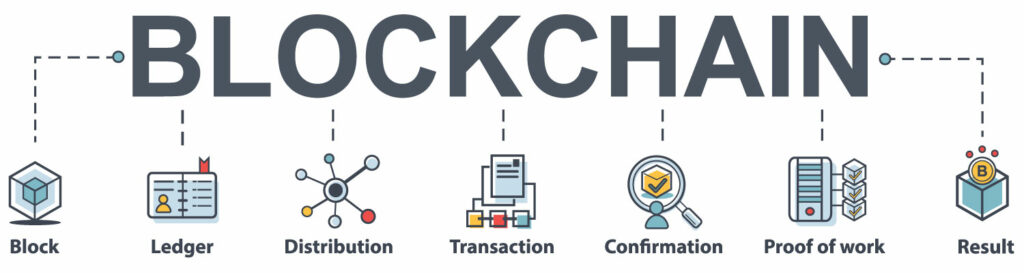

Blockchain technology has emerged as one of the most groundbreaking innovations of the 21st century, promising to revolutionize industries ranging from finance to healthcare, supply chain management to digital identity verification. At its core, blockchain represents a decentralized and immutable ledger system that enables secure and transparent peer-to-peer transactions without the need for intermediaries.

Key Features of Blockchain

- Decentralization: No single entity controls the blockchain. Instead, it operates on a peer-to-peer network, eliminating the need for intermediaries and enhancing trust among participants.

- Transparency: All transactions on the blockchain are transparent and publicly accessible. Anyone can view the entire transaction history, enhancing accountability and auditability.

- Security: Cryptographic techniques ensure the security and integrity of transactions on the blockchain. The decentralized nature of blockchain makes it resistant to censorship and hacking attacks.

Applications of Blockchain

Blockchain technology has diverse applications across various industries, including:

- Cryptocurrency: Bitcoin, Ethereum, and other cryptocurrencies leverage blockchain technology for peer-to-peer digital transactions.

- Smart Contracts: Self-executing contracts programmed on blockchain platforms automate and enforce contractual agreements without intermediaries.

- Supply Chain Management: Blockchain enables transparent and traceable supply chains, reducing fraud, counterfeiting, and inefficiencies.

- Digital Identity: Blockchain-based identity solutions offer secure and verifiable digital identities, empowering individuals with control over their personal data.

- Healthcare: Blockchain facilitates secure and interoperable health data exchange, ensuring privacy, security, and accessibility of patient records.

Challenges and Future Developments:

Blockchain technology has garnered significant attention for its potential to revolutionize industries and enhance various processes. However, like any emerging technology, it faces several challenges that must be addressed for widespread adoption. Here are some of the key challenges:

- Scalability: As the number of transactions on a blockchain network increases, so does the time and resources required to validate each transaction. Current blockchain platforms like Bitcoin and Ethereum have limited transaction throughput, leading to congestion during periods of high demand.

- Interoperability: With numerous blockchain platforms and protocols in existence, achieving interoperability between them is crucial for seamless data exchange and collaboration.

- Security Concerns: While blockchain is renowned for its security features, it is not immune to vulnerabilities and attacks. Threats such as 51% attacks, double spending, and smart contract bugs pose risks to blockchain networks and the assets stored on them.

- Regulatory Compliance: Compliance with existing regulations and legal frameworks presents a significant challenge for blockchain-based projects, particularly in highly regulated industries such as finance, healthcare, and supply chain.

- User Experience: Blockchain technology is often perceived as complex and challenging for non-technical users to understand and interact with. Improving the user experience and simplifying the process of onboarding users onto blockchain platforms is essential for mainstream adoption.

- Energy Consumption: Proof-of-Work (PoW) consensus mechanisms, used by blockchain networks like Bitcoin and Ethereum, consume significant amounts of energy to validate transactions and secure the network.

Addressing these challenges will require collaboration between industry stakeholders, regulators, and technology innovators to develop scalable, interoperable, and secure blockchain solutions that meet the needs of diverse use cases and industries. Despite the hurdles, the potential benefits of blockchain technology are vast, and overcoming these challenges will pave the way for its widespread adoption and integration into various sectors of the economy.